From Tracks to Towers: How Hong Kong’s MTR Shapes the City

Introduction

Towards the end of last year, I spent a few weeks in Hong Kong. Although it was due to unfortunate circumstances, it was nice to re-immerse myself in the things I miss—things like hairy crab, clay pot rice, freshly caught tropical seafood, a milder winter, and a lot of sunshine. I was also reminded of the city's exceptional public transportation. In Hong Kong, transit isn’t just a service; it’s a source of civic pride that is deeply ingrained in the culture and integral to the city’s architectural identity.

Michael Wolf’s photography captures Hong Kong’s density in striking detail—an almost dystopian sea of high-rises (Wolf). The city is incredibly dense, deeply flawed, and notoriously unaffordable, consistently ranking among the world’s most expensive cities, even surpassing London (Reuters).

Yet, beyond these critiques, my research has uncovered a creative approach to urban development often overlooked, especially when viewed through a Eurocentric lens. Despite its challenges in unaffordability and density, Hong Kong has built one of the most profitable and self-sustaining transit systems in the world. Today, I want to explore its Rail + Property model and the lessons it might offer for the UK.

Transit Culture & Systems

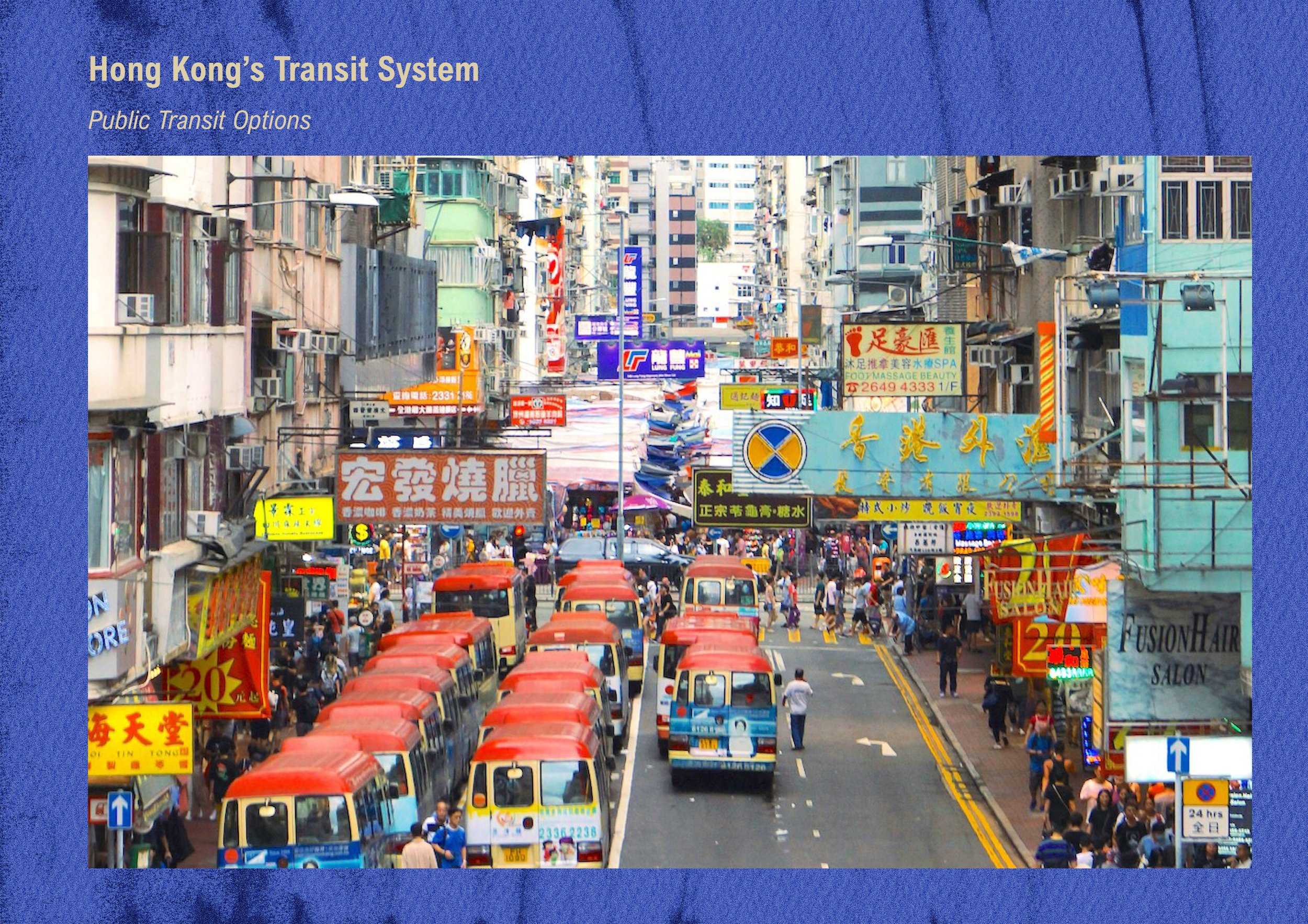

To get from Point A to Point B, there are lots of options—buses, minibuses, taxis, the famous double-decker trams, affectionately called the "Ding Ding."

At the heart of it all is the Mass Transit Railway (or, the MTR), a 12-line, 93-station system that serves the majority of the city’s 7.5 million residents. Every weekday, 5.9 million people take public transport—more than the entire population of Norway or Singapore (MTR Corporation). It’s so efficient, clean, and convenient that almost everyone uses it.

To contrast that with car ownership:

The UK has about 600 cars per 1,000 people, and the US nearly 800 per 1,000.

In London, the number drops to 240 cars per 1,000—but in Hong Kong, it's just 92 cars per 1,000 people (Statista).

If the US is defined by car culture, then Hong Kong is defined by public transit culture.

But what makes Hong Kong’s system unique is that it doesn’t rely on government subsidies. In most cities, transit operates like a public utility—serving people, but not making money. In the U.S., for instance, public transit is often seen as social welfare, primarily used by low-income groups and heavily subsidized by taxpayers (United States Department of Transportation, National Transit Database).

A key measure of financial sustainability is the Farebox Recovery Ratio, which shows what percentage of operating costs are covered by fares:

U.S. systems cover as little as 10% of costs, relying heavily on subsidies (United States Department of Transportation, Farebox Recovery Ratio).

Hong Kong’s MTR leads the world at 185%—meaning it not only covers its costs but generates profit to give back to the government (MTR Corporation).

Yet, fares remain affordable: £1.70 to cross Hong Kong Island, £5 from the mainland border to Central, and just 25p for a tram ride. This success isn’t just due to high ridership or efficiency—it comes down to how the MTR monetizes access to its greatest asset: the 90% of Hongkongers who use it (MTR Corporation).

Rail Plus Property

Here’s how the system operates:

For new rail lines, the government provides MTR with land “development rights” at stations or depots along the route. To convert these development rights to land, MTR pays the government a land premium based on the land’s market value without the railway (Planning Department).

MTR develops new rail lines and partners with private developers through a competitive tender process to build properties.

In return, MTR receives a share of the development profits, which may come as a percentage of total earnings, a fixed sum, or a portion of commercial property revenue. This value-capture model funds new projects while supporting operations and maintenance (McKinsey & Company).

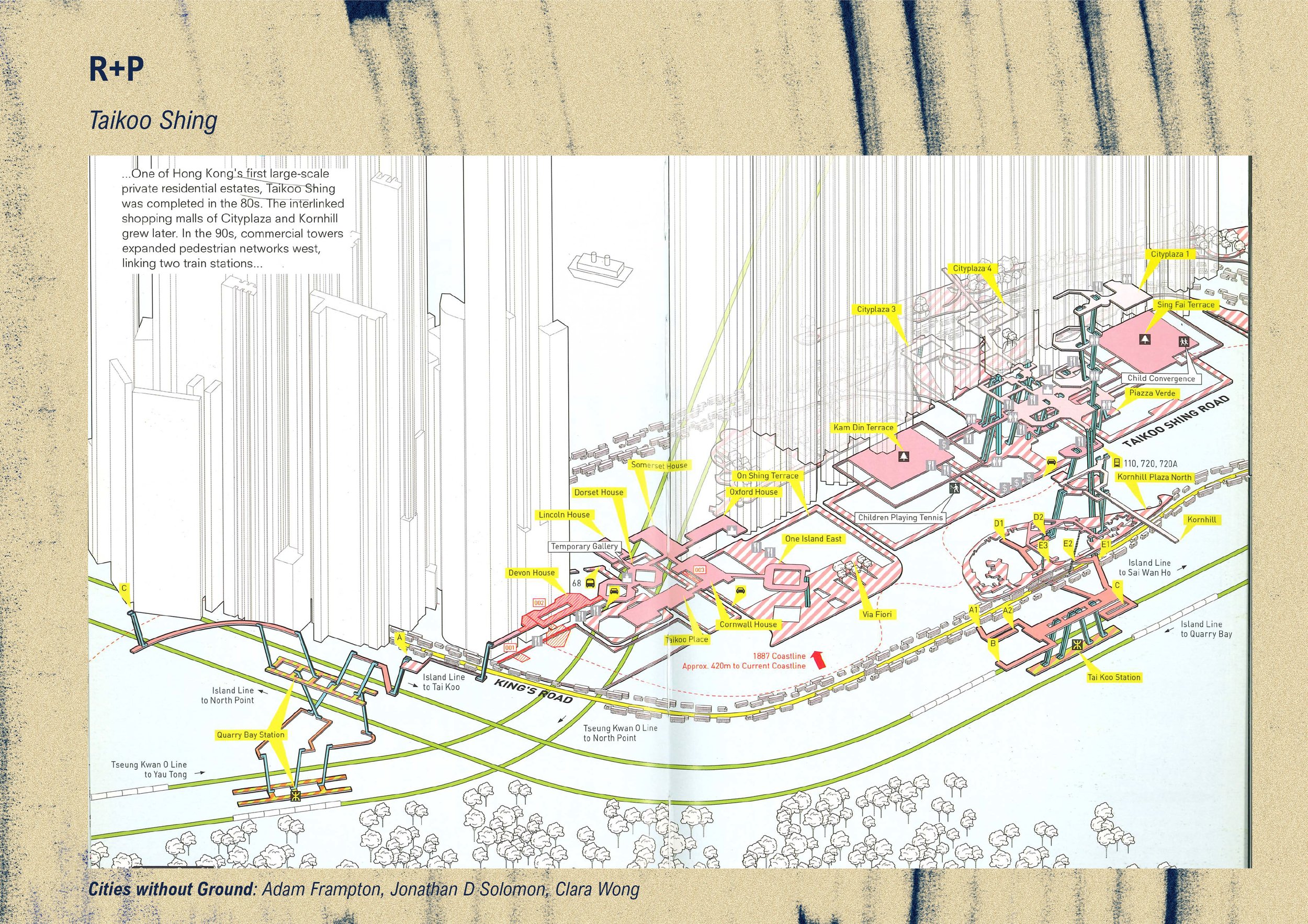

Beyond railway infrastructure, MTR profits from leasing and selling property, with over 1,400 station shops and ownership stakes in developments above and around transit hubs. Its portfolio includes Hong Kong’s tallest skyscrapers, the Four Seasons Hotel, the Ritz-Carlton, and 50 other projects (MTR Corporation). These Rail-plus-Property (R+P) developments create compact, pedestrian-friendly communities where residents can navigate the city without exposure to Hong Kong’s heavy rainstorms and typhoons—a convenience they often take pride in.

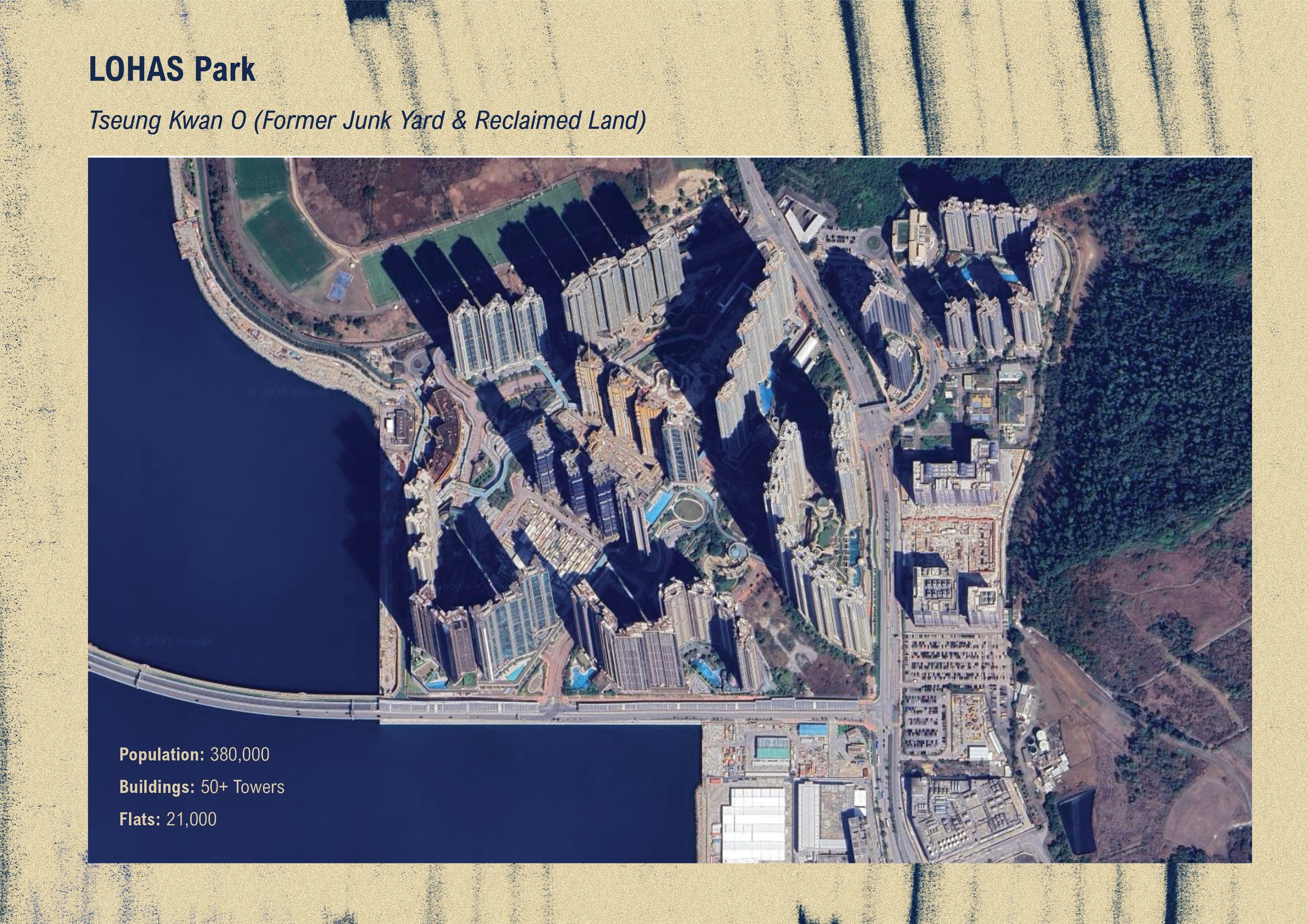

Revenues from Rail-plus-Property (R+P) developments above stations along MTR’s Tseung Kwan O line, for example, funded its extension to serve a new town that has since grown to 380,000 residents. The development includes a vast residential complex with 50 towers and 21,000 apartments, enabling people to live, work, and shop entirely within the MTR ecosystem (Planning Department).

This model is highly profitable. In 2018, MTR earned 8.2 billion HKD from fares but an even greater 12.7 billion HKD from property and commercial ventures (MTR Corporation). A portion of these profits is returned to the government, which holds a 75% stake, in the form of stock dividends (MTR Corporation). By minimizing reliance on government funding, the MTR operates as an efficient, market-driven enterprise, allowing it to maintain and expand its network with agility. At the same time, the government views public transit not as a financial burden but as a valuable revenue stream—one it is actively incentivized to enhance and improve (McKinsey & Company).

Housing Unaffordability

Hong Kong’s housing shortage isn’t due to a lack of space—75% of its land is green space, while only 7% is used for housing (Civil Engineering and Development Department). Some areas are too mountainous for development, but others, like the 420-acre Fanling Golf Course, remain underutilized despite dense high-rise congestion (Planning Department).

The real issue is economic. To attract businesses, Hong Kong caps income tax at 15% and relies heavily on land leases for revenue. With nearly all land government-owned, land sales contribute 27% of its income (Reuters). To keep prices high, the government releases land gradually rather than meeting demand. As a result, Hong Kong has some of the world's most expensive housing.

A two-bedroom flat in Hong Kong averages £1.3 million, significantly higher than London's £750,000 and the UK's £230,000 average (Zoopla). In Hong Kong, with an average property price of £26,200/m2 and a median annual salary of £23,000, an average worker can afford just 0.87 m² of living space (Census and Statistics Department). All of which underscore Hong Kong's pronounced housing affordability challenges

To illustrate how much £1,000 can buy in terms of living space in these three locations:

Hong Kong: 0.038 m² (38 cm²) – About the size of a standard iPad screen (10–11 inches diagonal).

London: 0.080 m² (80 cm²) – Roughly the footprint of a pair of men’s size 9 shoes placed side by side.

Greater UK: 0.304 m² (304 cm²) – Approximately the surface area of a standard office chair seat.

Both the government and MTR Corporation, with financial incentives to restrict land supply and inflate property values, play a key role in the housing crisis. As a result, most Hongkongers are forced to live in cramped conditions. In many ways, residents pay for their world-class transit system not just through unaffordable housing, but also through the control of the MTR—and by extension, the government—exercises over their daily movement.

Application in the UK

The UK faces challenges in public transport funding, housing shortages, and urban connectivity—issues the Rail + Property (R+P) model could help address (McKinsey & Company). However, key differences affect its feasibility. Unlike Hong Kong, where the government owns most land, UK land is largely private, making it harder for transit authorities to acquire property affordably before values rise (Planning Department).

R+P thrives in Hong Kong due to its unique conditions. The city’s dense population and limited land supply drive up real estate values, ensuring profitable developments (Census and Statistics Department). Residents are also accustomed to living near transit hubs and value the convenience of integrated railway and property projects (MTR Corporation). While Hong Kong’s extreme density guarantees high ridership and strong property demand, transit-oriented development in the UK would likely be viable only in major cities like London, Manchester, and Birmingham (McKinsey & Company). Additionally, the UK’s slower and more complex planning system further complicates large-scale, transit-led projects (Transport for London).

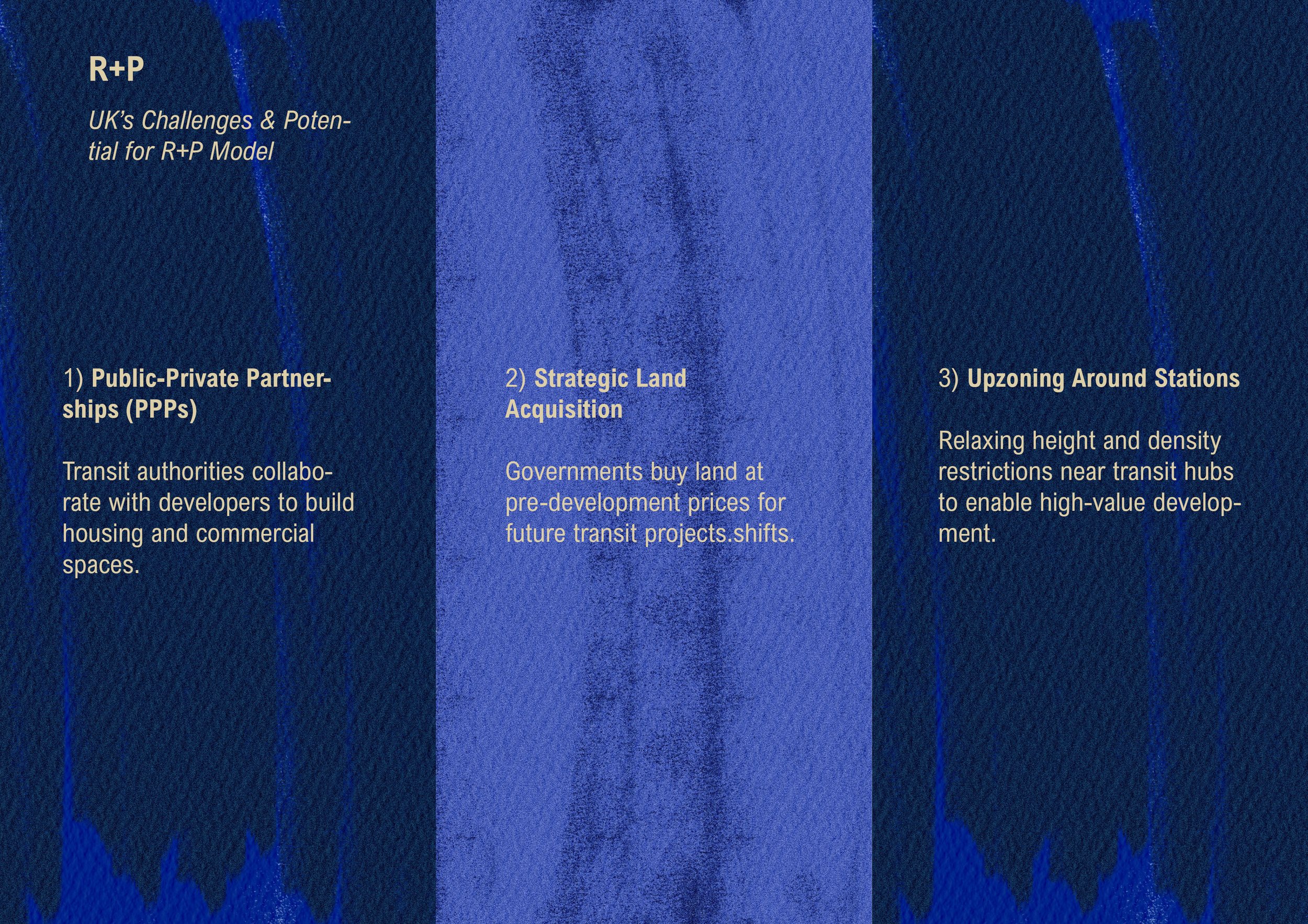

While fully replicating Hong Kong’s Rail + Property (R+P) model may be impractical, the UK could adopt key elements to strengthen transit funding through three strategic policies:

Public-Private Partnerships (PPPs): Transit authorities could collaborate with developers to build housing and commercial spaces around transport hubs, generating revenue for infrastructure (McKinsey & Company).

Strategic Land Acquisition: Authorities could purchase land at pre-development prices for future transit projects, capturing value appreciation over time (Planning Department).

Upzoning Around Stations: Relaxing height and density restrictions near transit nodes would encourage high-value developments, boosting revenue potential (Census and Statistics Department).

The R+P model offers a compelling approach to sustainable transit funding. If properly implemented, it could reduce the UK’s reliance on public subsidies, improve infrastructure, and expand housing supply (McKinsey & Company). Success requires a shift in perspective—seeing transit not just as a service but as a driver of economic and urban growth (MTR Corporation). By integrating transport and property planning, the UK can move toward a more efficient, financially sustainable, and well-connected urban future (Transport for London).

Conclusion

I’ve been accused of turning into a full-blown nationalist when talking about Hong Kong’s transportation. This MMM isn’t strictly about architecture, but it’s worth zooming out to the developer-level decisions that fund our work and shape our cities (Wolf). MTR isn’t just a rail company—it’s a global urban powerhouse, shaping London, Stockholm, Beijing, Sydney, and Shenzhen (MTR Corporation). Its success isn’t just about transit; it’s about strategic urban planning at scale (McKinsey & Company).

I used to dismiss this kind of architecture—dense, monotonous, copy-paste urbanism—but behind it are calculated decisions on land value, infrastructure, and financial viability (Census and Statistics Department). So, what is our role? We work within the frameworks developers set, but how do we push back, advise, and advocate for better outcomes? Even if we’re not making developer-level decisions, how do architects meaningfully engage with the forces shaping our built environment?

Meanwhile, in November 2024, TfL announced that the Elizabeth Line’s operating contract will shift from MTR to GTS Rail Operations Limited—a consortium of three Japanese rail companies—starting May 2025 (Transport for London). As a public transit enthusiast, I find this transition fascinating. MTR is world-class, but Tokyo’s metro is on another level—an absolute joy to experience (McKinsey & Company). With Tokyo Metro stepping in, I’m eager to see how the Elizabeth Line and surrounding areas will evolve and flourish under its new leadership (Transport for London).

Bibliography

Census and Statistics Department. Hong Kong Annual Digest of Statistics 2023. Government of the Hong Kong Special Administrative Region, 2023. www.censtatd.gov.hk.

Civil Engineering and Development Department. "Land Usage Distribution in Hong Kong." Civil Engineering and Development Department, https://www.cedd.gov.hk/filemanager/eng/content_954/Info_Sheet2.pdf.

Civil Engineering and Development Department. "Land Utilization in Hong Kong 2023." Civil Engineering and Development Department, 2023, www.cedd.gov.hk.

Frampton, Jonathan D., Naomi C. Hanakata, and Adam Frampton. Cities Without Ground: A Hong Kong Guidebook. ORO Editions, 2012.

Hong Kong Mass Transit Railway (MTR). Annual Report 2018. MTR Corporation, 2018. www.mtr.com.hk.

McKinsey & Company. "The Rail-Plus-Property Model." McKinsey & Company, 2024, https://www.mckinsey.com/capabilities/operations/our-insights/the-rail-plus-property-model.

Michael Wolf. Architecture of Density. Peperoni Books, 2012.

MTR Corporation. Annual Report 2018. MTR Corporation, 2018.

Padukone, Neil. "The Unique Genius of Hong Kong's Public Transportation System." The Atlantic, 23 Sept. 2013, https://www.theatlantic.com/china/archive/2013/09/the-unique-genius-of-hong-kongs-public-transportation-system/279528/.

Planning Department. "Land Utilization in Hong Kong." Planning Department, https://www.pland.gov.hk/pland_en/info_serv/open_data/landu/.

Planning Department. "Land Utilization in Hong Kong 2023." Planning Department, 2023, www.pland.gov.hk.

Reuters. "Hong Kong Budget Looks to Tackle Deficit Blowout Amid Economic Headwinds." Reuters, 25 Feb. 2025, www.reuters.com.

Statista. "Private Cars per 1,000 Population in Hong Kong 2009-2019." Statista, 3 Jan. 2024, https://www.statista.com/statistics/960015/hong-kong-private-cars-per-1000-population/.

Transport for London (TfL). "Press Release: Elizabeth Line Operating Contract Change." TfL, Nov. 2024, www.tfl.gov.uk.

United States Department of Transportation. Farebox Recovery Ratio of U.S. Transit Systems. Federal Transit Administration, 2023.

United States Department of Transportation. National Transit Database 2023. Federal Transit Administration, 2023. www.transit.dot.gov.

Zoopla. "Average House Prices in London and UK." Zoopla, 2024, www.zoopla.co.uk.